Steps You Should Consider To Lower Taxable Income

Understanding your taxes is not just about saving a few bucks here and there. It’s more about taking control of your financial future. As an employee, knowing how these taxes impact your income is a key part of building financial stability.

Learning effective strategies to lower taxable income can allow you to make informed decisions and maximize your earnings. If you’re looking to get the most out of your paycheck, these tax reduction strategies are worth knowing.

In this guide, you will discover the expert strategies and tax reduction techniques to help you lower your taxable income. You will learn tested and trusted tips, including how you can calculate your taxable income.

What Does Taxable Income Mean?

When an individual or business has an income, a portion of that income goes into taxes. The government and other legal governing bodies consider this portion for all tax deductions. For some people, the portion is high, while for others, they have lower taxable income.

The lower the taxable income, the lower the amount of deductions the government is able to make on your income. This means you actually save a couple of dollars on taxes that can be diverted to other expenses.

Compounded savings on taxes can also improve your overall financial status. Understanding how your taxable income is calculated and what contributes to lowering it is very important. You can better optimize your tax strategy and get the most out of your income. In taxable income, there are certain key deductions that are considered to influence how much you pay in taxes.

Knowing each of these deductions and how you can use them in your favor is an advantage. That way, you can take key, strategic steps towards legal reduction in your taxable income.

Deductions That Help Lower Taxable Income

In tax finance, there is something called allowable deductions. These deductions made to your gross income have an effect on your tax bill. Here are some of the deductions and how they impact your taxable income:

Donations

Employees or organizations that have a consistent history of charitable donations can use this to lower their tax income. These charities must be qualified and registered for it to be legally acceptable. If you have the records of your donations and a consistent, long-term history, you can claim the maximum deduction available.

Mortgages

This deduction applies to homeowners who pay interest on their home mortgage. This interest, when paid up to the limit allowed by the law, can be deducted. The result is a reduction in your taxable income.

State and Local Taxes (SALT)

These are taxes that an individual or a business pays at the state or local level. The one downside to this deduction is that it has its limits. However, it can still help you lower your taxable income. For this deduction, you need an accurate record of all payments made using the standard documentation process.

Student Loans

The student loan interest deduction allows you to subtract interest paid from taxable income. This deduction is considered an above-the-line adjustment with up to $2,500 deductible. Individuals with qualified student loans can claim it even if it is not itemized in deductions on the tax return.

Medicare

This deduction is binding on out-of-pocket medical expenses. You can deduct all healthcare expenses that exceed the set limit from your income. It means you can ease the burden of high medical bills while lowering your taxable income.

Retirement Contributions

This is one of the most powerful tools in tax finance and is very effective in lowering your taxable income. When you make contributions to accounts like 401(k)s or IRAs, you reduce your taxable income for that year.

Additionally, these contributions grow tax-deferred up until retirement. It means you reduce your taxable income by increasing your retirement contribution. The more contributions you make to retirement, the less you pay in taxes, with more long-term benefits on your income.

Other Deductions

You have more deduction options, though not as common as the others. They are also effective in reducing your taxable income. They can range from educational expenses to business-related expenses. Sometimes, even unreimbursed employee expenses can fall into this category. As long as you are up to date on all tax regulations and guidelines, you can claim these deductions.

These tax strategies might not immediately lower your taxable income. However, in the long run, you will start to notice compounding benefits. Ultimately, they help you secure your future financially.

How To Calculate Your Taxable Income

Calculating your taxable income lets you know exactly how much of your earnings will be deducted for taxes. This gives you a better understanding of your tax bill and informs you of the proper reduction process. The standard formula to calculate taxable income is:

Gross Income - Allowable Deductions (Standardized or Itemized)

It means you start with everything you have earned so far and then subtract it from allowable deductions. These deductions can either be itemized or standardized. Here is a simplified step-by-step breakdown to help you calculate your taxable income:

-

Step 1: Determine your gross income. This is the combination of all sources of income, such as wages, salaries, bonuses, interest, dividends, rental earnings, and self‑employment income.

-

Step 2: Calculate your adjusted gross income. These adjustments include retirement contributions, student loans, and health-related expenses. Once you subtract your gross income from the adjustments, you have your adjusted gross income.

-

Step 3: The next step is to apply your deductions. To do this, you need to subtract your standardized or itemized deductions from your adjusted gross income. The result would be your taxable income.

Practical Steps To Lower Your Taxable Income

Putting theory into practice is essential. Here’s a practical checklist to help you lower your taxable income effectively:

-

Review your tax returns frequently to know which deductions to claim and what gaps are in your records

-

Place a higher priority on retirement contributions. This is one of the most effective tax strategies for reducing taxable income.

-

Always have accurate and reliable records of all expenses, donations, and deductibles. You can use an app or software to track and keep these records.

-

Be very strategic about your income and expenses and time your deductibles well for when your income is higher.

-

Never underestimate professional advice from a tax finance expert. Schedule a consultation to get tailored tax strategies.

-

Adopt a tax management template or software to help you automate most of your tax reduction processes.

To Sum It Up

Lower taxable income means better financial planning. These innovative tax strategies will help you maximize your deductible expenses. It reduces the part of your income subject to taxes. By following these tax reduction tips, you can create a more secure financial future.

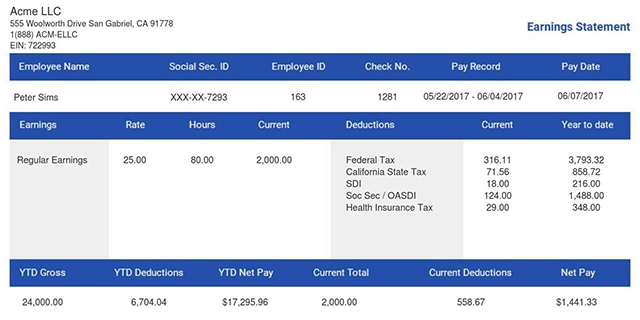

Try out our online pay stub tool to help you manage your finances and make smart tax decisions. Keep track of all your deductions and maximize every dollar to your advantage.

- 1. Enter Your Information

- 2. Select Your Favorite Theme

- 3. Download Your Stub!