IRS Red Flags That Trigger an Audit and How To Avoid One

In every tax season, millions of people in America do their taxes with the hopes of a hitch-free process. Some may even anticipate a refund. However, at the back of taxpayers' minds are three letters that give you chills: IRS.

Nowadays, audit rates are much lower than they used to be. The overall audit rate is now under 1% for individual returns. Still, some parts of the tax return are audit triggers.

In this article, we will identify top IRS red flags that can lead to an audit. You’ll also learn how to avoid them and keep the IRS out of your business.

How Do IRS Red Flags and Audits Work?

The Internal Revenue Service (IRS) tests people's tax returns. It is unclear how the algorithm that they use to pick the people they’ll audit works. Of course, it's probably as secret as the formula for Coca-Cola. Yet, a number of tendencies can be identified by relying on historical audit data and IRS behavior.

Contrary to what many people may assume, not all audits stem from suspected fraud. Some are randomly chosen as part of the IRS's National Research Program. This helps establish statistical standards for various income brackets. However, most audits occur due to certain figures or details on a return that deviate from norms. It may also be because of high-risk factors.

Top IRS Red Flags

These are the top red flags that may bring an audit your way:

-

Unreported Income

This is one of the common tax filing mistakes that causes issues. It is a frequent and possibly the easiest to prevent audit sign. Some people fail to report all sources of income that are taxable. As you’re getting your income and tax documents, the IRS is also getting them. These documents are automatically cross-checked with what you have reported in their computer systems.

You may also receive a letter audit for some sources that don’t seem important. Examples are income received from an old brokerage account or money earned through a part-time job.

This applies to incomes of all types, including those from shares, gigs and cryptocurrency transactions. In fact, the 1040 form now has an improvement. It wants to know if you did any digital asset transactions. Being dishonest comes with certain risks for the individual. It raises the level of audit risk to an undesirable level.

-

Significant Income Fluctuations

Gross income fluctuations between one year and another are also potential IRS red flags. That said, it is possible that such changes are legitimate. So, the IRS may simply want assurance that the change is because of a shift in the true economic conditions. They want to be sure it's not because of the income that you didn't report.

You may be in a situation where you have had a major income change. It is wise to write a letter of explanation to the IRS in advance before filing the tax return.

-

Disproportionate Deductions

Another thing that can bring audits your way is large deductions. Not just that, it has to be too large compared to how much you earn or can earn. This will attract attention from the IRS. The agency compares your deductions against statistical norms for your income bracket and profession.

Out of all the deductions, one can be considered a special issue. Also, if you make too many contributions to charity, it may attract attention, which can lead to an audit. The risk is higher where the amounts are too high in comparison to your income.

Additionally, when a donation exceeds $500, one has to file Form 8283. Donating any valuable asset generally requires an appraisal.

-

Home Office Deduction

The home office deduction has been, for many years, considered a major red flag. But then, there have been a lot of changes to the tax law. Also, there's the increasing popularity of telecommuting. So, scrutiny has recently been reduced.

Nevertheless, this deduction is thoroughly scrutinized by the IRS. They need to be sure that part of your home meets the “exclusive and regular” use criterion. This is for a home-based business.

A common mistake is claiming an area that may be occasionally used for working. For instance, the dining table. Some may also claim that a proportion of the space in the house is too large.

-

Claiming Refundable Tax Credits

Such incentives allow the IRS to send money back to you. The way they operate even makes it possible for you to get back more than the amount you paid. One popular example of these types of tax credits is the Earned Income Tax Credit (EITC).

There's a high error rate with these claims. So, such returns come with more scrutiny when claiming these credits.

-

Mixing Personal and Business Expenses

There is always scrutiny when it comes to business expenses. This is because some people end up mixing it up with personal expenditure. Vehicle usage itself is one of the problem areas. For example, it is not advisable to claim 100 percent business use of your car. Some even do this for the only car they own. That’s a way to easily call for an audit.

It is important to maintain documents that separate business and personal expenses. You also need to have records of travel deductions for automobiles.

How Can You Avoid Being Audited?

The best piece of advice that can be given with regard to audits is not to avoid the auditable deductions. It is to develop a good habit of recordkeeping. Make sure you have the necessary documents to back up every single thing that’s on your return.

Tax season doesn’t just start when January comes around. You need to prepare and keep records throughout the year. This is very important for those in business or self-employed individuals. Keep and save records of the receipts and bank statements. Store invoices and any other relevant documents that support your income and deductions.

You can use applications or software to track documents like receipts. This makes it easier to deal with such scenarios. Some enable you to track your expenses throughout the year. So, it's easy when preparing to pay taxes. If by any chance, you need to be audited, it can be handled. But that's only if you have the necessary documents.

To Sum It Up

IRS audits are not very frequent, but you need to know the main IRS red flags. This information can become the basis for correct filing. The best action is not to avoid any legal deductions and credits. The correct way is to ensure the correctness of the deductions and credits. Following that, keeping adequate documentation and readiness to back up all these items on the return. Thus, taxpayers can reduce the risk of an audit. At the same time, they can still claim the allowances to which they are entitled.

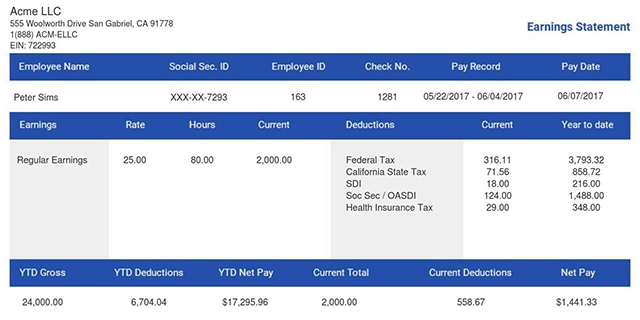

Stay audit-ready with our pay stub creator. Our platform helps you generate accurate, professional pay stubs. This ensures your income records are well-documented and tax-compliant. Avoid IRS red flags and file with confidence. Check it out today!

- 1. Enter Your Information

- 2. Select Your Favorite Theme

- 3. Download Your Stub!