A Guide to the Internal Revenue Code - Section 162(m)

Are you up-to-date on Section 162(m)? Does it apply to you or your business? Recent changes broadened the number of corporations and the types of executives that Section 162(m) of the Internal Revenue Code covers. Find out here about Section 162(m). Learn what it means for executive compensation, corporate taxes, and more.

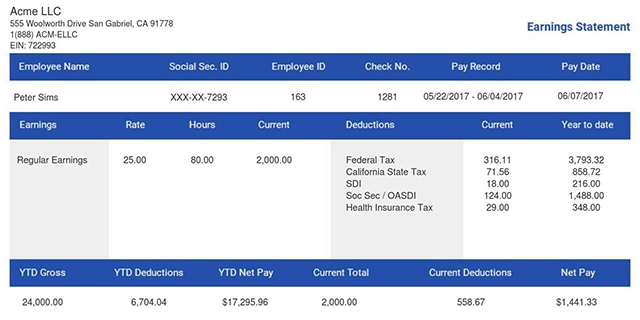

Also read: Payroll Tax Vs Income Tax - The Ultimate Guide

What Is Internal Revenue Code Section 162(m)?

Section 162(m) is a section of the US tax code. It regulates how much executive compensation a company can deduct from its corporate income taxes. Section 162(m) of the Internal Revenue Code first came into effect in 1994. Congress thought that corporations were paying their executives too much. This compensation wasn't tied to how well the corporation was doing.

Many people have blamed Section 162(m) for the rise in executive compensation. Criticism of the provision led Congress to reform it in 2017. In fact, the mean total compensation for CEOs increased 9% per year from 1994 to 2016. It rose 10% for executives other than the CEO during the same period. However, salary as a percentage of total compensation decreased.

The use of incentives increased. Equity compensation, like stock options, ties the executive's wealth to the company's performance.

Also read: What Is FUTA Tax - All You Need To Know

Tax Cuts and Jobs Act Reform Of IRC Section 162(m)

Congress passed the Tax Cuts and Jobs Act (TCJA) in 2017. This law makes significant changes to Section 162(m) of the Internal Revenue Code. The changes took effect on January 1, 2018. The TCJA affected several parts of IRC Section 162(m). The main changes include:

- Expanding the number of public companies that have to follow the deduction limit

- Expanding the number of executive officers that the rule covers

- Eliminating the exception for commission-based and qualified performance-based compensation

- Eliminating the IPO transition

A "grandfather rule" protects written, binding contracts that were in effect on November 2, 2017. The old Section 162(m) rules apply to such contracts.

Expanded Definition of Publicly Held Corporations

The Tax Cuts and Jobs Act changed the definition of a publicly held corporation. Section 162(m) now includes any corporation that as of the last day of its tax year either:

- Is an issuer of any class of securities required to be registered under Section 12 of the Securities Exchange Act, or

- Is required to file reports under Section 15(d) of the Exchange Act

The new definition includes domestic corporations with publicly traded debt. It now includes some foreign corporations. Publicly held subsidiary corporations are also included.

Expanded Definition of Covered Executives

Before the changes to Section 162(m) of the Internal Revenue Code, the compensation deduction limit in each fiscal year applied to four executives at a corporation. The limits affected the person serving as CEO of the corporation on the last day of the fiscal year. The three highest-paid executives who weren't the CEO or the CFO were also covered.

The Tax Cuts and Jobs Act broadened this definition in several ways. Section 162(m) now applies to anyone who served as the CEO during any part of the fiscal year. The CFO is no longer exempt. Any executive who served as CFO during any part of the fiscal year is also a covered executive. Section 162(m) continues to apply to the next three highest-paid executives after the CEO and CFO.

The types of executive officers found in the Securities Exchange Act are the only ones who can qualify as classified under Section 162(m) In addition, executives classified as covered in one year keep that classification. The executive remains a covered employee of the corporation even after the employment relationship ends or the person dies.

The "once-covered, always-covered" rule applies retroactively. Any executive classified as covered in any tax year after December 31, 2016, remains covered. The number of covered executives for a corporation can increase rapidly.

Also read: What Qualifies As Proof Of Income?

Compensation Subject To The Deduction Limit

The deduction limit continues to be $1 million per covered executive. However, corporations can't exclude performance-based or commission-based compensation anymore. Compensation includes the total remuneration given to an executive for services performed in any capacity, including as a director or consultant.

Many corporations will lose some tax deductions under the new Section 162(m) rules. However, they may benefit from increased flexibility regarding executive compensation. Under the old IRC Section 162(m) rules, the process to qualify performance-based compensation for a tax deduction was lengthy and expensive. Corporations no longer have to follow those procedures.

They can change their compensation practices to lower administrative expenses. They can give their boards more flexibility. Executive performance goals are no longer limited to quantifiable measures like business productivity. Companies can now use subjective performance measures, like increasing social responsibility.

Some investors fear that companies will become less transparent in how they compensate their executives. The major trading exchanges still require companies to have independent compensation committees, though. Shareholder approval of equity compensation plans also remains a requirement.

Elimination Of The IPO Transition

The Tax Cuts and Jobs Act eliminated a transition period that used to be available for companies that became publicly held. Under the old rules, compensation that a company paid to executives and disclosed to prospective shareholders before the company became public was exempt from the deduction limit. The transition period generally lasted for three years.

Companies are now subject to the Section 162(m) deduction limits for the taxable year when they become public. The limits apply to compensation paid before the initial public offering but during the same taxable year. The new rules apply to corporations that become publicly held after December 19, 2019.

The rules apply no matter how the company becomes public (initial public offering, spinoff, etc.).

Grandfathered Arrangements Under Internal Revenue Code Section 162(m)

The Tax Cuts and Jobs Act includes a grandfather rule. The new version of Section 162(m) doesn't apply to written, binding contracts that were in effect on November 2, 2017. A key provision of the grandfather rule is that the contract can't have had any "material modifications" since that date. Material modifications include changes such as:

- Automatic renewal

- Increasing the amount of compensation (other than for cost-of-living)

- Accelerating the payment of compensation

Corporations will need to be very careful to avoid making material modifications to a contract if they want to keep grandfathered arrangements.

Compliance With Section 162(m) Of The Internal Revenue Code

The changes to Section 162(m) are likely to have a significant impact on how businesses handle executive compensation. Corporations may face a higher tax bill at both the federal and state levels. Compensation procedures can now be more flexible, though. To simplify your tax season, check out our paystub creator as we'll help take the stress out of your tax preparation.

- 1. Enter Your Information

- 2. Select Your Favorite Theme

- 3. Download Your Stub!