What Is Gross Monthly Income?

Your gross monthly income is one of the first numbers you'll come across when managing your money. It usually appears on your employee pay stubs, tax forms, loan applications, and budgeting apps. With this, you must understand that your gross monthly income is important to you as a worker.

So, whether you're earning a salary, working hourly shifts, freelancing, or running your business, you need to know about it. Your gross income gives you the total amount you bring in.

It could affect how you budget, whether you qualify for loans, and how much you owe in taxes. It also affects how you want to plan for the future.

In this article, we'll break down what gross monthly income is, how to calculate it, and what it includes. All these would explain why your monthly gross income is important when managing your finances.

What Does Gross Monthly Income Mean?

Your gross monthly income is the total amount of money you earn in a month before anything is taken out. This refers to your taxes, pension deductions, health insurance, or any other withholdings you earn. Gross monthly income can come from several sources, and it typically includes:

-

Salary or wages (whether you're paid every month, twice a week, or every hour)

-

Bonuses and commissions (common in sales or performance-based jobs)

-

Freelance or side-hustle income

-

Rental income (from properties you own)

-

Investment income (like dividends or interest from savings/investments)

However, don't get confused, as your gross income is different from the money you take home. That's called your net income, which ends up in your bank account after all your deductions have been made. For example, you may earn $5,000 monthly as your salary, and after taxes and deductions, you receive $3,800. Your gross monthly income is $5,000, while your net income is $3,800.

Your gross monthly income is necessary to approve your loans, rent an apartment, and lower your credit limits. They are usually not based on your net income, as lenders want to know how much you actually earn. Understanding what counts as gross income helps you see your full earnings. This then enables you to make better financial decisions.

How To Calculate Gross Monthly Income

How you can calculate your gross monthly income simply depends on how you earn your income. It usually varies, depending on whether you're a full-time employee, an hourly worker, or self-employed. However, if you don’t know how or where to start, you can use a gross monthly income calculator. It helps to save you the stress of calculating it manually.

Here's a simple way to calculate it without a monthly gross income calculator, depending on your work type:

-

If You Earn a Monthly Salary

Employees who earn salaries have the easiest means to calculate their gross monthly income. If you have a fixed annual salary, you just need to divide it by 12 months. Let's say you earn $72,000 a year, so to find your gross monthly income, it's:

$84,000 ÷ 12 = $7,000

This means that your gross monthly income is $7,000. Even if you choose to work overtime or even take a few days off, this doesn't change. Your salary is fixed.

If you earn a monthly salary and have a side hustle, you can calculate it in a similar way. Let's say David is a school teacher who also works as a driver for a rideshare service on weekends. From his full-time teaching job, he earns $48,000 in a year, which is:

$48,000 ÷ 12 = $4,000 per month

David also earns about $600 each month from his rideshare service. His pay depends on his driving time. To calculate his gross monthly income, he needs to add both amounts that he earns:

$4,000 (teaching) + $600 (rideshare) = $4,600

So, David's gross monthly income is $4,600.

-

If You're an Hourly Worker

To calculate your gross monthly income, you can do this by using this formula:

Hourly wage × average hours you work weekly × 52 weeks ÷ 12 months

So, let's say you earn $22/hour and you work 32 hours per week, it's:

$22 × 32 = $704/week

$704 × 52 weeks = $36,608/year

$36,608 ÷ 12 = $3,050.67/month

So, your estimated gross monthly income is about $3,050. However, if your work hours change often, they can be different. You'll have to take the average number of hours you work weekly over a few months to get a better estimate.

Another example is Emily, who works as a kitchen assistant and earns $18/hour. She works 40 hours a week. However, when it's really busy, she does about 10 hours of overtime per month, which is usually paid at time-and-a-half. Here's how her base income breaks down:

$18/hour × 40 hours/week = $720/week

$720 × 52 weeks = $37,440/year

$37,440 ÷ 12 = $3,120/month

Now, let's add the overtime:

-

Overtime pay = $18 × 1.5 = $27/hour

-

10 overtime hours/month = 10 × $27 = $270/month

Add that to her regular gross income, which is:

$3,120 + $270 = $3,390

Therefore, Emily's gross monthly income is approximately $3,390, assuming it's consistent over time.

-

If You're Paid Biweekly or Semi-Monthly

These can be a bit confusing because they sound the same, but actually, they’re not. If you work biweekly, you get paid every 2 weeks, and in a year, you'll receive 26 paychecks. If you work semi-monthly, you only get paid twice a month and receive 24 paychecks in a year.

Let's say your biweekly paycheck is $2,000:

$2,000 × 26 = $52,000/year

$52,000 ÷ 12 = $4,333.33/month

Now let's say your semi-monthly paycheck is also $2,000:

$2,000 × 24 = $48,000/year

$48,000 ÷ 12 = $4,000/month

The way you get paid impacts your total monthly income. This is even when it's the same paycheck in every amount.

-

If You're Self-Employed or a Freelancer

If you run a business, do contract work, or freelance. It can include writing, design, photography, and consulting. Your income may change each month. You'll add all your total income over the last 12 months to calculate your gross monthly income. Then, divide it by 12.

Let's say over the past year, you earned $4,000 from freelance writing and $2,000 from photography gigs. The total amount you earn is $6,000. Therefore:

$6,000 ÷ 12 = $500/month

Your estimated gross monthly income is $500

If you see that your income is growing or changing, you can always use a shorter average. For example, one over the past 6 months, so that it can show how much you truly earn. You just need to make sure that you're consistent while using this method.

Another example is Jason. He is a freelance web developer. His income changes each month based on his clients. In the last 12 months, he earned 3 big projects at $4,000 each. Also, he has had other smaller jobs, where he earned $8,000. Therefore:

(3 × $4,000) + $8,000 = $20,000

To calculate his average gross monthly income:

$20,000 ÷ 12 = $1,666.67

So Jason's gross monthly income is around $1,666, even though he may earn more or less in some months.

Why Is Your Gross Monthly Income Important?

You might be wondering why you need to know your gross monthly income, which is valid. It is one of the first things that is required when you want to do certain things as an employee. Here's why it is important:

-

Loan and Mortgage Eligibility

It is useful while applying for a loan, like a mortgage, car loan, or even a student loan. Lenders want to ensure that you can afford to repay your loan. To figure that out, they look at your debt-to-income (DTI) ratio. This compares your monthly debt payments to your gross monthly income.

If your gross income is $5,000/month, and your total monthly debt payments are $1,500. Your DTI would be:

$1,500 ÷ $5,000 = 0.3 or 30%

Most lenders prefer a DTI that is lower than 43% to approve you for a mortgage. So knowing your gross income gives you a clear picture of how much debt you can take on. This helps your chances of getting your loan approved.

-

Rent Approvals and Housing Affordability

Landlords and property managers also examine your gross income to see if it meets the “3x rent” rule. It is also known as the 30% housing rule. Your gross monthly income should be at least three times the monthly rent.

For example, if you want to rent an apartment costing $1,200, your gross monthly income should be around $3,600. This lets them know that you can pay your rent consistently.

-

Credit Limits, Insurance, and Benefits

Credit card companies also use your gross income to determine the credit limit that you have. If you have a higher income, it can often lead to a higher spending limit and better interest rates. It's also used when you apply for insurance or want to see if you qualify for government benefits. It could be benefits like healthcare subsidies, student aid, or public housing.

Gross vs. Net: Budgeting Implications

Knowing the difference between gross and net income can really impact your budget. While they're both important, they serve different purposes. This is especially when it comes to spending, saving, and planning your financial life.

You can think of gross income as the full paycheck your employer promises you on paper. Net income, on the other hand, is what actually lands in your bank account.

For example, let's say you're offered a job with a gross monthly income of $5,000. However, it reduces once you subtract taxes, Social Security, health insurance premiums, and maybe a 401(k) contribution. You might end up taking home $3,700 or even less.

These are common deductions that reduce your paycheck:

-

Social Security and Medicare

-

Health, dental, or life insurance

Why Net Income Is Needed for Budgeting

When it comes to managing your day-to-day expenses, net income is your budget. This is the money you have left for rent, groceries, savings, and fun activities. The popular budgeting framework, like the 50/30/20 rule, relies on net income, which is:

-

50%: for needs like rent, bills and groceries

-

30%: for wants like fun activities and entertainment

-

20%: for savings and debt repayment

You can't use gross income for these because it doesn't account for how much you can afford. If you try to budget from your gross income, you may overspend without even realizing it.

Why Gross Income Is Needed

So if net income is better for budgeting, why then do you still need to care about your gross income? This is because gross income is usually used by:

-

Lenders and banks: for loans and credit

-

Landlords: for rent applications

-

Government programs: to assess your eligibility

-

Employers: for offers and compensation packages

Gross Income vs. Earned Income

While filling out your tax form or applying for a loan, you may have come across the term “Earned income”. It may sound like gross income, but it’s not the same. Knowing the difference is important. This is when it comes to managing your finances, especially during tax season.

Earned income is much more specific and refers to the money you earn for working. This includes your salary, hourly wages, commissions, bonuses, or freelance work. If you're self-employed, earned income is your profit after you deduct business expenses. Passive income, such as dividends, rental income, or interest, isn’t earned income.

Gross income, on the other hand, just refers to all the money you earn before any deductions. It could also include rental income, dividends, interest from your savings, royalties, and business profits. It could also be your side hustles, and even alimony in some cases.

Knowing the difference between both helps when calculating your taxes. Your gross income can be used to determine your Adjusted Gross Income (AGI). This then affects your tax rate and your eligibility for credits and deductions. For example, let's say you earn:

-

$60,000 from your full-time job (earned)

-

$3,000 from a part-time gig (earned)

-

$2,000 from investments (not earned)

Your gross income is $65,000, but your earned income is $63,000. This is important when claiming credits like the Earned Income Tax Credit (EITC). This only considers money you've actually worked for.

Also, knowing the difference helps you plan better. It affects how much tax you owe and what tax benefits you qualify for. It also determines if you qualify for health care subsidies or child tax credits.

Common Mistakes Involving Gross Monthly Income and Tips To Avoid Them

Always be careful when calculating your gross monthly income. If you aren't careful, you can make a mistake while budgeting or managing your finances. These are some of the most common mistakes and how you can avoid them:

-

Forgetting Irregular Income or Seasonal Variations

If you earn extra money during some months, it's easy to overlook that when calculating your income. The tip is to just not think about the last month. Instead, look at your total income over the past 12 months and divide it by 12. That way, your slow and busy months balance out and you get a more accurate monthly average.

-

Miscalculating Biweekly vs. Semi-Monthly Pay

This mistake is common, and it confuses even long-time employees. If you're paid biweekly, you receive 26 paychecks per year. If you're paid semi-monthly, you get 24. You may think that it doesn't matter, but it changes your monthly income calculation.

You can learn to calculate your gross income for biweekly and semiweekly pay. Try not to mix them, as using the wrong one can either overstate or understate your income.

-

Overlooking Bonuses, Commissions, and Side Hustles

If you earn commissions from sales, occasional bonuses, or you freelance, this is common. Many people forget to include these when calculating their gross income. So, any income before deductions that you earn regularly should be part of your gross income. Even if it's not every single month. You can keep a simple income tracker or spreadsheet to help you total everything up.

-

Mixing Up Gross and Net Income

It is also a common mistake to use your gross income to limit your spending, especially when your take-home pay is lower. This could lead to you overspending. The solution to this is for you to use your net income instead to make your budget. You only use gross income for loans, debt-to-income ratios, or job offers.

In Summary

Calculating your gross monthly income always gives you a clearer view of your finances. As a salary earner, or if you're self-employed and juggling multiple income streams, this helps greatly. You will be able to clearly understand what you earn before considering your deductions and taxes. With your gross monthly income, you can make smarter choices when setting goals that could impact your finances. It could also simply be while you're planning your next big move.

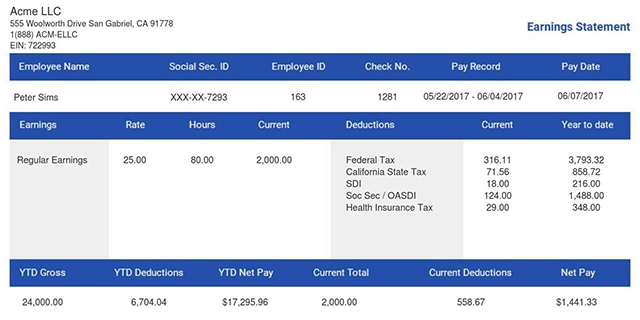

With our professional pay stubs generator, employees, freelancers, and business owners easily see their gross income, deductions, and net pay. We've got you covered if you need proof of income for any applications or just staying on top of your finances. Start generating accurate paystubs with us today!

- 1. Enter Your Information

- 2. Select Your Favorite Theme

- 3. Download Your Stub!