How To Use Pay Stubs for Loan Applications Without a Hitch

Most people look for a loan to finance the purchase of a car, buy a house, and many other reasons. In all cases, the lender will need to establish the person’s income. They need to know the borrower can repay when the time comes.

Pay stubs are an essential part of this process. They are regarded as legal proof of your income. Pay stubs enable loan providers to understand your ability to manage finances responsibly.

In this article, we’ll explain how to use pay stubs for loan applications. You’ll also learn about other components of the proof of income process.

Why Use Pay Stubs for Loan Applications?

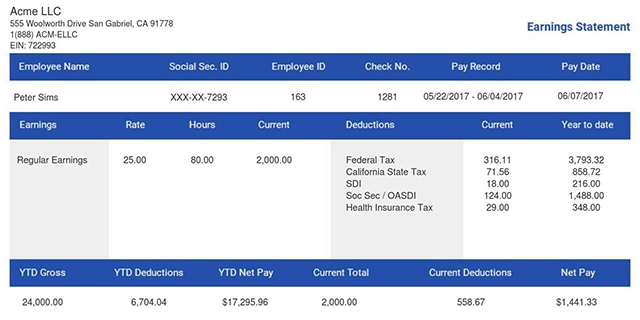

Pay stubs are official documents employers give employees to explain their pay. It shows their earnings and deductions for a particular period of pay. Examples of items in the stub are gross pay, taxes, insurance, and net pay.

For loan applications, pay stubs are a prime document that shows exactly how much someone is earning. Then, you can determine how capable the person can meet their financial obligations. They are useful to prove that you will easily meet the required demands for loan repayment.

When applying for a loan, the lenders use this information to evaluate your debt-to-income ratio. This helps them determine the amount of the loan to approve for you.

Other than the current earnings, pay stubs also demonstrate employment steadiness. This is another important consideration that the lenders look out for. You may present the check stubs from the same employer. This indicates that you show more job security, which means less risk to the lender.

How Banks and Lenders Use Pay Stubs

Lenders check pay stubs very closely while evaluating the loan applications. This evaluation is for the following reasons:

-

Income Verification

The main purpose is proof of income. The lender needs to be sure that you can pay the proposed loan amounts. You should know that lenders will compare your gross income with the required loan amount. They’ll also review your outstanding loans to arrive at the DTI ratio.

-

Employment Stability

Stability in employment can be determined based on the pay stub. They want to see continuity in employment with the same employer. This assures the lenders of stability and, therefore, low risk. Lenders will always prefer when the borrower has been at the same job for at least two years.

-

Withholdings and Deductions

Subtractions from gross income are how your true income helps the lenders understand your position. It enables them to determine the proportion of your earnings that are already spoken for by other obligations.

-

Identity and Employment Verification

They may also use your pay stubs to check your identity. Other times, it’s to verify your employment details. They can check if the information on it is consistent with other documents you have submitted.

Types of Loans Requiring Pay Stubs

Different sorts of loans demand pay stubs as part of the application, though the precise rules may vary:

Mortgage Loans

Mortgage loans need the most significant amount of documentation from an applicant. It is common for the provider to ask for pay stubs of not less than 30 days or up to 3 months. They may also ask for W-2 forms for up to one to two years.

With tax returns, you may need to submit for the last two to three years. This helps them check the applicant's past earnings and finances thoroughly.

Auto Loans

Auto loans constantly demand the latest pay slips, usually from the last month. They just need to be sure that you will be able to meet your current and future expenses. That includes the car’s monthly repayment.

Personal Loans

Personal loans can be more lenient with their conditions. That depends on the amount of money borrowed or the type of personal loan. Some lenders may require only one or two pay stubs. For larger sums, they will need other proof of income documents for that as well.

Student Loans

Student loans and refinancing may require applicants to provide proof of income. Private lenders need to ensure that the borrowers are well-equipped to make the necessary payments. This can be while in school or afterward.

How Many Pay Stubs Do You Need?

Different loan types and the lenders’ policies determine the number of pay stubs. When it comes to submitting a pay stub for mortgage loans, you need recent stubs. Most require copies for the last month or 30 days, while others require 3 months.

However, they usually ask for many other accompanying documents. This results from the long-term financial and contractual relationship between the provider and the customer.

The number of pay stubs for auto loans is usually fewer. You may provide the most recent one or two pay stubs for most applications. Depending on the loan amount and credit score, the number may increase.

Some personal loan sources may only need your most recent pay stubs. This is mainly when you apply for a small loan or have a good credit score. Large loans may require additional documentation from the borrower. That is apart from the application form.

The frequency of your pay schedule is also a factor that affects the requirements. For instance, a person may receive biweekly checks. Then, two check stubs will represent a month’s salary. Applicants paid by the week may be asked to submit four stubs to show their monthly income.

The best case scenario is always to have as many recent documents as possible. Even more than the most basic ones you think you might need. Prepare additional pay stubs in case the lender requires additional information.

Alternative Proof of Income Documents

When there are no pay stubs, many lenders allow you to use other proof of income documents, such as:

W-2 Forms

W-2 forms give a detailed account of your income for the year. They are usually required along with pay stubs when applying for a mortgage. They give a wider perspective of income earned throughout the fiscal year compared to pay stubs.

Tax Returns

A summary of your sources of income will be revealed by tax returns. This includes income from self-employment, investment, and rental houses. Tax returns are very useful for self-employed applicants. Mortgage lenders often request for one to two years worth.

Bank Statements

Pay slips can be further supported or, in some cases, substituted by bank statements. These statements contain records of deposits by your employer. This shows proof of receiving an income as stated on the application form.

Employment Verification Letters

Documentation from the employer can help verify your position and remuneration. These are particularly useful for newly employed individuals. Mostly, they don’t have several pay stubs yet.

Bottom Line

Pay stubs for loan applications are essential for a hitch-free process of borrowing. Through them, a lender proves income and employment security. Requirements differ depending on the type of loan and the lender. However, pay stubs when applying for a loan can help a lot in the loan approval process. Self-employed persons and those with non-traditional income have other considerations. They should understand other ways to prove income. This will assist in overcoming any challenges they may encounter.

Simplify your loan application process with professional pay stubs from our pay stub generator. Accurately showcase your income details to meet lender requirements. Let’s help you boost your chances of approval. Visit today to create reliable and detailed pay stubs with ease.

- 1. Enter Your Information

- 2. Select Your Favorite Theme

- 3. Download Your Stub!