Do You List Credit Cards on the Loan Application? - The Full Guide

Having been responsible for your finances, you probably want to apply for available credit. However, are you unsure if your scoring models qualify for a new car loan, mortgage process, or other financial product?

Probably, you are not sure what your best lender considers when looking at your creditworthiness. Are you wondering what to fill out on the assets and liabilities section of your application for home loans?

Credit card debt is mostly termed as an unsecured liability. The more your cards, their varying terms and credit limit, the more significant your debt to pay. However, the most significant problems are mortgages or financing auto loans. Most lenders tend to reject card debts if they are too high or a cycle of irregular payment history lowering your credit scores.

Since credit card accounts offer credit, their liability stays open indefinitely. Credit bureaus track and report this debt alongside all relevant borrowing activity. Read on to learn whether to list credit cards on your application.

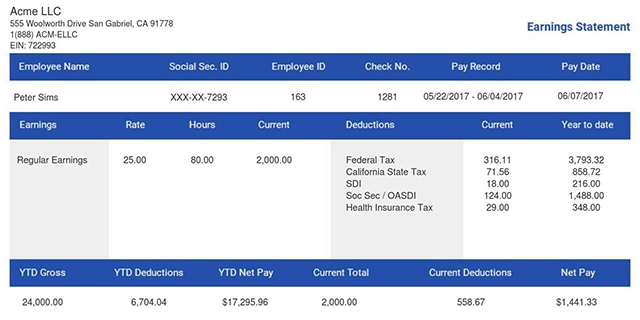

Also read: How To Get A Check Stub For Loans?

- Why Do you list your Credit Cards on your Loan Application?

- How Does My Credit Card Activity Affect the Fate of My Mortgage Application?

- Will A High DTI Stop You from Qualifying for a New Loan?

- Is Having No Credit Card Accounts Better for a Loan?

- Will Paying Down My Credit Card Debt Improve My Loan Approval Chances?

- When Reviewing an Application, Do Lenders Look into My Credit Card Spending Habits?

- Can a Loan Request Be Affected by Having Too Many Credit Cards?

- Why Should I Disclose All My Credit Cards when applying for a Loan?

- Conclusion

Why Do you list your Credit Cards on your Loan Application?

Unless you've got thousands of dollars in savings, you'll need an available credit to make any big purchase, say in a house, land, or a vehicle. However, you'll notice the request for your assets and liabilities within the application, listing what you own and owe.

An asset is anything that's yours, including businesses or invested money. Liability consists of a debt or payment such as car loans or your credit card balances.

Your creditor's concern revolves around your ability to repay the loan in a reliable, timely manner, often monthly.

Therefore, alongside anyone acting as a guarantor, co-signer, or co-borrower, you'll be asked to list the current values of assets, including your bank balance, despite being a new account. In addition to ascertaining your employment status and income, you should provide this information honestly.

Having some savings works well towards assets to provide some comfort to your loan lender.

But if your liabilities or debts exceed your income, a lender might be concerned your cash reserves won't last long. For that reason, you'll be asked about your monthly spending and a list of your ongoing debt. That includes credit card balances, student loans, any loans, and other recurring payments like child support or alimony.

Also read: Did Your Credit Score Drop Off After Paying Off Debt?

How Does My Credit Card Activity Affect the Fate of My Mortgage Application?

Before approving your loan application, lenders consider attributes like a good credit score to determine what terms to offer for these financial products.

Some of these factors include your income outstanding or recurring debts, such as your credit cards or mortgage balances. In addition, you may need to provide verifiable documents such as tax returns or paystubs for income reporting, which isn't part of your credit report.

Lenders are always determined to legally verify you can afford to make your personal loan payments. Any outstanding monthly financial obligations such as credit card repayments and your income are part of this equation. They'll use this information to calculate;

-

Your Debt-to-Income Ratio or DTI

Monthly debt payments like credit cards are compared to your income by the DTI, and how it will be affected by a new loan is reviewed. While a mortgage broker or lender will calculate this differently, a maximum allowable debt to income ratio, such as 43%, can be set to qualify for mortgage approval.

-

Payment to Income Ratio or PTI

The PTI determines how much your income goes towards repaying loans. Your Payment to Income ratio may be set at 15% and 20%.

With a high income and lower loan repayments, you can achieve favorable DTI or PTI ratios, best for an application. However, if your income is insufficient to cover the credit payments, lenders may choose to reject your request. What happens if you're paying too much on your cards?

Depending on the personal loan you're applying for, there's a maximum annual income to debt or payment ratio if you're to meet your creditor's approval. Both DTI and PTI furnish your credit applications as part of your initial application process.

Also read: Do Banks Verify Pay Stubs

Will A High DTI Stop You from Qualifying for a New Loan?

Unless your DTI is way higher than what mortgage lenders are obligated to allow, having a credit card loan doesn't necessarily mean you don't qualify. Considering two different ratios, a creditor divides your monthly debt by your pretax or gross income. These include;

The Front-end DTI ratio divides your gross income against monthly household expenses and loan repayments. For your loan or mortgage approval process and better credit mix, you need your DTI to stay below 28%.

Back-end DTI ratio, your total loan repayments, including your credit card payments, are considered. For this, maintain a level below 36% if your lender is to approve your personal loan application.

The back-end DTI is more significant to lenders, and you'll have a hard time qualifying for a personal loan where it's risen above 36%. However, neither the back nor the front-end DTI considers installment debt that's almost paid off or monthly expenses such as food and gas.

Also read: What is the average credit score?

Is Having No Credit Card Accounts Better for a Loan?

As one of the common forms of revolving credit, you're offered numerous benefits by credit cards.

For example, you can utilize their limits and lower payments and interest rates responsibly to debunk your creditworthiness. In addition, most providers, whether old or new credit cards, offer rewards like spending points or cash backs that you can use to pay outstanding balances.

Your preferred lender will look at credit history from bureau analysis reports, including your relevant borrowing activity. That means you'll be building out a favourable credit profile with proper use of cards, such as timely repayments. In retrospect, negative profiles can result from having high balances, delinquent payments, or numerous hard inquiries over a short time.

Your credit card accounts for a significant part of your profile's credit utilization, so they're highly influential in determining your FICO score. Bureaus track your credit card companies' bank accounts, evaluating your total debt by aggregating itemized trade lines.

This implies it's rare for identity theft to occur, although it's through a family member profile. Then, they reach your credit utilization ratio by dividing the aggregate amount of credit mix limits on your cards.

The credit utilization ratio is a significant factor used by credit report bureaus to determine your credit score. Credit card payment history includes delinquency detracts from your profile while timely remittances build on it, helping you qualify for more favorable lending terms.

Before making any new credit card applications, you can improve your chances of success by paying down parts of outstanding credit card balances.

Also read: Cash Back Credit Cards

Will Paying Down My Credit Card Debt Improve My Loan Approval Chances?

Before applying for a loan, pay down your credit card debt to improve your credit score. But since lenders calculate DTI based on your monthly payment amounts, positive credit card balances may be of little help. So, be careful of methods of paying down that will harm rather than improve your card utilization ratio and credit score.

For example, introductory 0% APRs offered by a new credit card issuer will cause a slight hit to your credit score. These are called hard inquiries on your account, and they will negatively reflect your utilization ratio. But while paying off credit card debt doesn't much affect your DTI, it may be enough to place you below the favored 36%.

It's unnecessary to have an excellent credit score to qualify for personal loans or mortgages with a competitive interest rate. Paying off some credit card debt does raise it, but an average credit score of at least 620 is sufficient for you to qualify for some personal or housing loans.

An additional 1% of your loan's value buys a few points to reduce your interest rate by one percent, which is a good investment in the long term.

When Reviewing an Application, Do Lenders Look into My Credit Card Spending Habits?

You must prepare for the application process, understand expectations, and prepare the requisite documents. For example, your lender will look at your spending and saving habits, which is apparent through any credit card activity you've engaged in. In addition, creditors gain access to credit bureau reports that help them understand the state of your personal finances.

While your finances demonstrate that you can be trusted with a loan, signs of excessive or untimely spending don't reflect positively with your lender. They'll reject your application as you aren't ready to handle the responsibility that comes with significant credit. One of the aspects personal loans providers take time to evaluate is adding up your recurring and outstanding debt.

Frequently relying on credit cards to make large purchases negatively affects your credit score or FICO score. Moreover, failure to make timely monthly payments on any card will signal financial irresponsibility to lenders. As such, it's a good idea only to avoid impulse buying and to use your credit card only when it's indispensable.

Can a Loan Request Be Affected by Having Too Many Credit Cards?

Having credit cards or some other form of sustainable debt is a positive indicator of your being a responsible borrower. But owning multiple cards can make your lender cautious about extending additional credit facilities.

You can calculate your credit commitment by finding Debt Service Ratio or DSR. Find this by dividing your monthly net salary by your credit or mortgage payment obligations. The percentage of this ratio tells your lender how much of your income is used to pay off debts, and the lower it is, the better.

That's helpful to determine if you can handle another line of credit and pay for it reliably.

Also, lenders stay wary of your loan intentions unless you can rapidly justify taking up too many financial commitments. Accumulating debt over a short period signals your poor financial management, and you may need to provide concrete proof. Whether you disclose how many credit card accounts you have, that information is available when your loan officer runs a credit check.

You should review your credit report before making an application for a personal loan. You'll find a comprehensive breakdown of outstanding debts, financial blips, and existing loans. There could be an aspect that you're unaware of, and you could contest for a resolution before applying for further credit.

Why Should I Disclose All My Credit Cards when applying for a Loan?

Undisclosed debt only bogs down your mortgage approval, as your lender will have to work through attempting to resolve the issue. It shows irregularities in your financial health but affects approval, especially if you've taken on more debt recently. New debt throws off your DTI and FICO score, bringing it higher than the 36% favoured for instalment loans.

In today's loans provision industry, your lender will dig deep into your bank statements and credit history to discern qualifications such as with a home loan. You can't get away with not disclosing or listing your credit cards if you're to have any chances of getting a loan.

For instance, your mortgage broker or provider will run credit reports during and after your mortgage application process or even after closing. Withholding credit card information puts you in a not-so-complementing light with your lender, impacting your personal loan application.

Conclusion

Credit cards are the best form of obtaining a loan, and your card activity is crucial to the level of your credit score. It's an excellent borrowing tool that helps consolidate a favourable creditworthy profile if you use them correctly.

Reach out to expert Paystubs generating services that you can check online and print as proof of income. You'll also track your salary information, overtime, taxes, and more, just like it appears on this site.

- 1. Enter Your Information

- 2. Select Your Favorite Theme

- 3. Download Your Stub!