How To Prepare Your Accounts For New Hires - Full Guide

Whether you’re hiring someone on contract, a remote worker, or a freelance agent, new hires are a critical business investment and expense at the same time. Once you’ve identified the need to hire extra help, the next question that arises is how that will affect your accounts. Deciding on a number that’s favorable to you and the new hire is quite a delicate balance.

You have to consider the new hire’s potential value to the business, current market rates, and what you can afford. Your accounts determine if you’ll settle on a fair wage or you’ll push the compensation boundaries further. Imagine going through the interviewing process, picking the best candidate only to realize they’re out of your reach, compensation-wise.

That can be pretty shattering and a waste of time and resources. So how do you ensure your accounts are ready for new hires? This article is a practical guide to help you strike a good balance between your new hires and your accounts.

Step 1: Prepare your business account

This is the time to get your accounting records and a calculator because you’ll need to do some math. If you’re not familiar with how to prepare ledger accounts, it may also be an excellent time to learn. As you do your calculations, here are the things you need to keep in mind:

-

Costs related to new hires go beyond a salary: Does your business offer perks and benefits to employees, such as catering for lunches or health insurance? Do you need to get extra space, devices, or equipment with the new hires? The cost of maintaining an employee usually goes far beyond the salary package you offer. Keep in mind that there are payroll taxes as well that you need to contribute as an employer.

-

The costs need to fit in your budget: Look at your budget, previous profit trends, and the projections for the next year or thereabout. Is there any room to cover costs related to new hires, and how much is it? Consider the high and low business seasons. This is crucial so that you can understand if the hiring project will be sustainable.

-

Consider your profit margins: How much money do you actually make, and how much of it is the profit? When you’re able to put a figure on it, it will help you understand if the business is in a position to hire. You’ll also have an idea of up to how much you can afford while still leaving enough to cater to unforeseen issues.

Step 2: Establish the new hire’s potential value

Account preparation goes beyond what you’re going to invest in your new hires in terms of wages and other expenses. It’s also what they bring to the table. Depending on the designation you’re looking to fill, let your accountant help you come up with an estimate of how much value the team member will bring.

It can be directly for posts such as marketing and sales or indirectly for roles that boost efficiency in the business. For instance, you might have been losing customers because your customer service is lacking. Hiring a good team to transform this function and keep customers in and revenue flowing is indirect value to your business.

On the other hand, you might hire a sales team to sell your products or services, directly boosting sales and revenue.

Also read: 8 Steps To Create An Effective Employment Development Plan For Your Small Business And Its Benefits

Step 3: Determine the affordable and appropriate salary range

As mentioned elsewhere, new hires are a significant business investment. You’ll find it easy to prepare your account if you have a salary range in place. This calls for identifying and clarifying the job descriptions of new hires. Outline what you need them to do to add value to your business.

Depending on what gap you’re looking to fill in your team, skills, and experience, these are helpful questions to help you set a suitable salary range:

-

What is the highest amount the business can afford to pay and under what circumstances? Determining a top range is essential, but you need to have conditions for when and to what kind of candidate it applies to. This leaves you with little or no cushion for negotiation or increment. In addition, the new hire’s potential value should range at the top as well.

-

What amount can the business afford without straining the accounts? This will help you get the low-end salary range. You can set this range for those individuals who meet the minimum requirements, at least. Having a lower range lets you have room for raising the salary as the employee grows. It also allows your business to have a cushion amount or a negotiation range if the hire asks for a higher amount.

-

What’s the market rate for the post? Even while your accounts may determine what amount you pay to your new hires, you also need to consider what competitive salaries other businesses are offering. People looking for work mostly research rates beforehand, so they’re likely to know the market rates and are ready to negotiate to their desired amounts.

Unfortunately, if you’re unprepared, you might be caught off guard by a new hire’s salary proposal. Worse still, this may force you to give a package you weren’t at all prepared to give. As you mark your range and keep to your budget, remember that being competitive is essential. Please do your research early enough and do it well.

Look at what the employment laws say about minimum wage, overtime, and other compliance issues. Go to local job boards to see what range your competitors offer for roles similar to those you’re looking to fill.

Step 4: Let your accounts determine what you can afford

The whole point of carrying out the above is to ensure the accounts are well prepared for the new hires. When you have looked at your budget, profit trends, revenue projections, and market offers, you can set a realistic salary range. Try and find where these items overlap to get clarity on the compensation terms you need to offer your new hires.

Depending on where your bottom and top salary ranges fall, you can decide if your hire will be at the entry, middle, or top level. But if your range isn’t good enough for the average market compensation, consider other things such as hiring interns, contract workers, or opt for perks instead of a higher salary.

Step 5: After hire account preparations

After getting a competitive salary range and onboarding new hires, the journey is far from over. You need to consider how you’ll be paying the salary, withholding taxes, and other benefits to your new hires. Setting up and processing the payroll is a continuous job whether you settle on full time or part-time employment.

When your business is hiring, you need to consider withholding taxes, as some of them will affect your accounts in some way. If you already have other employees, you should be aware of the following five withholding taxes types that come with every hire:

-

Social Security tax: You have to contribute 6.2% of gross income on your account as the employer as the new hire contributes the other 6.2% to help them earn their social security credits.

-

Medicare tax: Commonly referred to as the hospital insurance tax, you need to contribute another 1.45% of your hires’ gross income, which affects your account somehow.

-

Federal tax withholding: You need to know how much you’ll be withholding and how much your business will contribute to the Internal Revenue Service (IRS) as income tax. Keep in mind the employer share withholding tax you’ll need to contribute depending on your new hires’ earnings. To help you get the correct amount to withhold in federal taxes, let your new hires complete Form W-4. The form enables you to know the right amount to withhold in taxes.

-

Federal Tax Statement: As the employer, it’s your responsibility to fill Form W-2 that details employees’ total annual income and taxes withheld.

-

State and local taxes: Some states also require you to withhold taxes from your hires. The same case applies to local governments.

Also read: Payroll Tax Vs Income Tax - The Ultimate Guide

Step 6: Include new hires in the payroll

You’ll need to include your new hires in your payroll processing system. This is where you’ll prepare the gross earnings of your new hires, calculate and make deductions, and generate paychecks and pay stubs. If your preferred method of paying your hires is a direct bank deposit, you’ll need to ask what is the account name for each to enable you to remit their earnings.

The process of paying your hires includes everything from tracking the hours worked, tax withholding and other deduction calculations, and prompt sending of paychecks. You also need to consider filing taxes on a monthly or quarterly basis, depending on the size of your business.

In Conclusion

Preparing your accounts for new hires is crucial in ensuring that your business can handle the additional expense. As much as new hires are an investment, they’re also a significant business expense. However, you can create a balance between your income and expenditure and come up with a suitable compensation plan for new hires favorable to the company and hires alike.

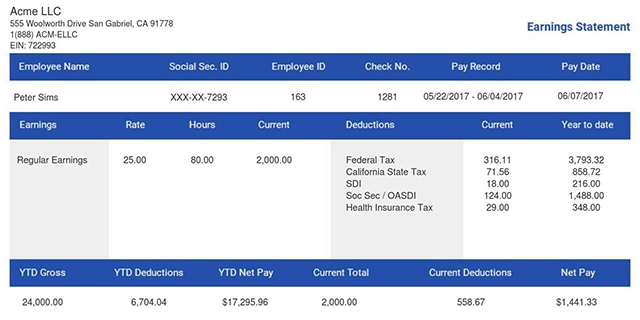

It is imperative that new employees can access their pay stubs so they can keep them for their own records also.

- 1. Enter Your Information

- 2. Select Your Favorite Theme

- 3. Download Your Stub!