Proof of Income for a Mortgage - The Full Guide

Buying a house is a goal many people dream of accomplishing. Browsing the internet or going out with a real estate agent to view potential properties is an exciting starting point for the process of homeownership, but it’s only the tip of the iceberg when it comes to the steps needed to achieve this objective.

Certainly, it’s important to know what you’re looking for in a home. But for most, the real starting point is obtaining a mortgage pre-approval.

Seeking a mortgage pre-approval or mortgage loan can be daunting. There are many documents a homebuyer will need to provide to the lender as proof of income, leading to a host of questions. How many pay stubs for mortgage pre-approvals? What should they include? What about W-2s and tax returns?

Read on for the basics of the mortgage pre-approval process and the number and types of documents a mortgage lender will likely require to get you started on the road to homeownership.

Also read: Are Home Improvements Tax Deductible?

- What Is a Mortgage Pre-approval?

- Why a Mortgage Pre-approval Is Important

- Do All Homebuyers Need a Mortgage pre-approval?

- What’s Involved In Obtaining a Mortgage Pre-approval

- Documents To Provide as Proof of Income for a Mortgage

- Proof of Income Documents for Self-employed Homebuyers

- Other Proof of Income Items

- Format of Proof of Income Documentation

- Next Steps in the Mortgage Pre-approval Process

- Using the Pre-approval Letter

- Completing the Mortgage Approval Process

What Is a Mortgage Pre-approval?

A mortgage pre-approval is the maximum dollar value of the home loan (or credit limit) that the mortgage company is willing to approve for you based on their evaluation of your financial position. Essentially, it’s your home-shopping budget. The pre-approval will dictate the maximum dollar value limit of your home purchase and give an idea of the size of the down payment needed to acquire the loan.

A similar term is a pre-qualification, which is only an estimate of how much of a loan a homebuyer may be able to get approved by the lender. Essentially, a pre-qualification is an estimate of creditworthiness rather than a commitment to a specific credit limit.

A pre-qualification doesn’t require the extent of documentation or the exploration of the homebuyer’s credit history that a pre-approval does. As such, it doesn’t carry the weight with sellers that the pre-approval will.

Why a Mortgage Pre-approval Is Important

First, it gives the homebuyer a budget to work with, which will naturally limit the range of potential home choices. A pre-approval will set realistic expectations for the size of mortgage payments a homebuyer can afford, saving time and heading off disappointment.

Secondly, the pre-approval gives the homebuyer an advantage when putting in a contract on a home, especially in a competitive seller’s market.

If a seller has a choice to accept a contract from a pre-approved buyer, the seller can feel more confident that the contract will close on time at the negotiated price. This prevents missed selling opportunities if a mortgage cannot be obtained for the contract price.

Do All Homebuyers Need a Mortgage pre-approval?

Most homebuyers in today’s market seek pre-approval for the reasons stated above: to know their budget limitations and to have an advantage when putting in a contract on a home. It's also important to know your numbers, such as your debt-to-income ratio and credit score, before shopping.

That being said, it isn’t always mandatory to have a pre-approval. It’s possible to put in a contract on a property without one, but there are risks for the homebuyer. There's the possibility that the mortgage company won’t give the homebuyer a mortgage for the contract price of the home, causing frustration for everyone involved.

It’s also a risk when putting in a contract with a seller. The seller may choose not to accept the contract without a pre-approval in a competitive real estate market, dashing the buyer’s hopes of owning that dream home.

What’s Involved In Obtaining a Mortgage Pre-approval

There are several items that lenders consider when giving a pre-approval. They look at income, credit score, and employment history to evaluate whether to give a pre-approval and the amount of the loan a homebuyer will be pre-approved for.

Mortgage lenders typically research the credit history, and the potential homebuyer has the burden of providing income and employment information and verification.

The biggest component of a mortgage pre-approval for a potential homebuyer is the burden of proof of income. The mortgage company wants to verify all sources of income over time to assist in calculating their risks of loaning funds to the homebuyer. They want to ensure that it’s very likely that the homebuyer will pay back the loan on schedule to make their business model succeed.

Documents To Provide as Proof of Income for a Mortgage

A potential homebuyer will need to provide several documents to the mortgage company to verify income to receive a mortgage pre-approval or loan. The list below contains some of the most commonly required documents for W-2 wage earners.

-

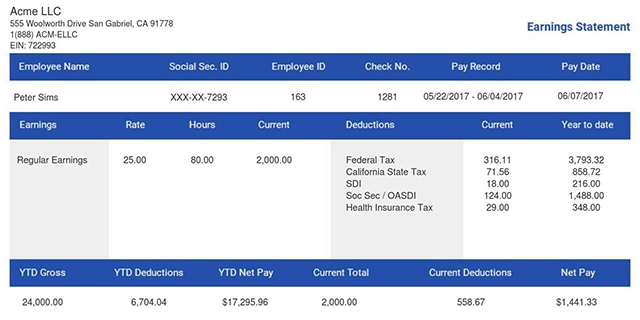

Pay Stubs

Typically two stubs covering the most recent pay periods are sufficient for a W-2 wage earner. They must show year-to-date as well as current period income to qualify. Self-employed home buyers must provide alternate documents in place of pay stubs.

-

IRS Form W-2

For most homebuyers, mortgage lenders will require the W-2 forms from the previous two tax years to verify an income history. This is to establish a pattern of income and to use it as a comparative reference to the current pay stubs to support a continued income stream. Again, self-employed homebuyers will provide alternate documents to establish their income histories.

Also read: Submitting a W2 Correction Request

-

Federal Tax Returns

For W-2 wages earners, an IRS Form 4056-T will need to be signed to authorize the mortgage lender to access the previous two years of federal tax returns. The returns will corroborate income and alert the lender to additional income streams aside from the amounts found on the W-2s.

-

IRS Form 1099

If a portion of homebuyer income is earned as commissions, the lender will require copies of IRS Form 1099 NEC from the previous two years to verify amounts and calculate an estimate for future commissions.

Interest and dividend income proof will come from the 1099-Int and 1099-Div forms, respectively. If a homebuyer has significant investment income to include, IRS Forms 1099-B will need to be provided. These forms summarize investment gains and losses for the tax year.

-

Proof of Income Letter

In the event the homebuyer has recently changed jobs, a letter may be requested to verify current and ongoing employment. With a more established work history, this won’t likely be necessary.

-

Passive Income

Depending on the source, a homebuyer must provide documentation of passive income sources to include them. Income from child support, social security, disability benefits, pensions, alimony, and other passive sources will have different documentation requirements such as a benefits letter or divorce decree.

Proof of Income Documents for Self-employed Homebuyers

The proof of income documentation requirements for employees is fairly straightforward. Employer-provided documents and tax returns constitute the bulk of the proof required. Complications arise when a homebuyer is self-employed.

While some of the documentation is the same, self-employed homebuyers have a more involved level of proof of income requirements. There are additional items required to complete the financial picture for this set of homebuyers. Following are some of the more common documents required for self-employed home buyers.

-

Tax Returns

The self-employed homebuyer must provide not only the last two years of personal tax returns but two years of business tax returns as well. Schedule K-1 may also be necessary if the business is a partnership.

Also read: How Do You Calculate Net Pay?

-

Bank Statements

In place of pay stubs, self-employed home buyers typically provide both personal and business bank statements as part of their documentation.

-

Year to Date Profit and Loss Statement and Balance Sheet

To evaluate the current state of the business, a lender will want to see how the business is currently faring compared to previous years. The mortgage company looks for a trend of steady or increasing income to feel confident in any credit line they may extend. Declining income will require additional explanation.

Other Proof of Income Items

If the homebuyer has recently received a significant sum of money in anticipation of a down payment on a home, additional documentation will be required to verify the source of the income.

Lenders request records of these transactions to ensure that the amount in question truly does belong to the homebuyer and is not an off-record loan that needs to be repaid. Following are some examples of documentation for common situations of this nature.

-

Gift Letter

If a parent or other family member gifts a large sum to the homeowner to be used towards a down payment, lenders typically require a letter from the source of the gift stating that the amount is truly given with no expectation of repayment.

-

Bill of Sale

If the homebuyer sells an asset, such as a boat or motorcycle, to raise funds for a down payment, a bill of sale will be required to prove that there is no loan involved in the transaction.

Format of Proof of Income Documentation

Traditionally, a homebuyer would need to provide paper copies of documents. With so many employers now providing electronic services such as direct deposit of paychecks and banks issuing electronic bank statements, some homebuyers may not receive paper copies of check stubs and other income documents.

Typically, electronic versions of these items are now widely accepted to accommodate the ever-growing trend of digitization.

Next Steps in the Mortgage Pre-approval Process

Once a homebuyer has provided all requested documentation, it’s time to move forward with the rest of the pre-approval process.

The lender will use the provided documents to verify and analyze income. Credit reports will also be pulled and reviewed for calculations including the debt-to-income ratio, a number that informs the size of the loan the homebuyer will be pre-approved for.

After compiling all of the requested financial information from the homebuyer in the mortgage system, the lender will then calculate their risk and decide on an extension of credit for a mortgage.

Using the Pre-approval Letter

Once the lender has given a pre-approval, it’s time to shop for a home. Homebuyers can use the amount on the pre-approval as a realistic guide for their home shopping budget. When it’s time to put in an offer, the pre-approval letter should be included with the paperwork submitted to the seller so it can be taken into consideration as they consider whether to accept.

Completing the Mortgage Approval Process

After a seller accepts an offer, the full mortgage approval process will begin. A complete mortgage application will be compiled. Once the lender researches and analyzes all of the information provided and receives an appraisal, final mortgage documents will be ready to sign to complete the purchase of the property.

With a pre-approval in hand, homebuyers can feel more confident that their home selection is within their budget and that their mortgage loan will be approved for the purchase of the house they plan to call home. Homebuyers who complete this important first step pave the way for a smooth and positive home buying experience.

- 1. Enter Your Information

- 2. Select Your Favorite Theme

- 3. Download Your Stub!