How To Save Tax On Your Salary [7 Methods]

We would all like to pay less tax, but it’s a reality for all income earners that a chunk of their salary goes to the IRS. We take a look at how to save tax on your salary in ways that are completely legitimate and legal.

Contribute To An IRA

An individual retirement account is a great way to simultaneously reduce your tax burden in the present and plan for your future. There are two main types of individual retirement accounts: a traditional IRA and a Roth IRA.

The contributions made to a traditional IRA are deductible from taxable income and so reduce the amount of federal income tax that will be owed. In the meantime, the retirement fund will be growing tax-free until you reach retirement age.

Roth IRA contributions are paid after tax is paid on your salary, but the account is also tax-free and can be withdrawn tax-free on retirement.

Tax-deductible contributions can be applied to traditional IRAs right up until tax day. The limit for contributions to an IRA is $6,000 annually.

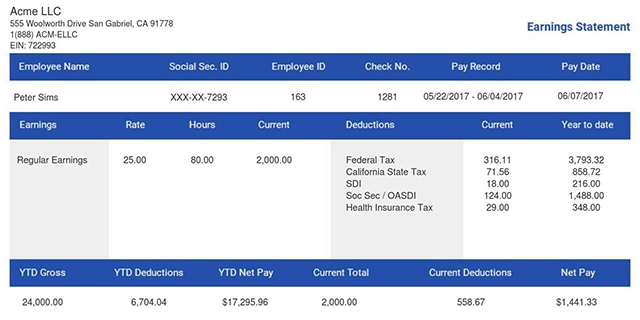

Also read: Payroll Tax Vs Income Tax - The Ultimate Guide

Open A Health Savings Account

For those with a high deductible health care plan, making contributions to a health savings account is a good way to reduce your taxable income. An HSA is a tax-exempt account that is used to pay your medical expenses.

Contributions are tax-deductible, growth is tax-deferred, and withdrawals are tax-free when used for qualified medical costs. With a self-only high deductible health coverage, the cap for contributions is $3,650; for family coverage, the limit is $7,300.

Those over the age of 55 can contribute an extra $1,000 to their HSA. You can open a health savings account with your employer if they offer one or alternatively at your bank or various financial institutions.

Any balance that remains in your HSA at the end of the year can roll over indefinitely.

Also read: 8 Steps To Create An Effective Employment Development Plan For Your Small Business And Its Benefits

Put Money In Your 401(k)

Contributing to your 401(k) is a popular way to reduce taxable income while also saving for your retirement. You will not be taxed on contributions that are diverted directly from your paycheck to your 401(k).

The maximum amount you can contribute to a 401(k) is $20,500 per year. Taxpayers over 50 years of age can add an extra $6,500 to that amount. Most employers offer 401(k)s, but if you are self employed, you can open your own.

Those who are on low to moderate income can claim the Retirement Savings Contribution Credit when they participate in a retirement plan such as a 401(k).

This is a non-refundable tax credit and can be claimed on top of the normal tax deduction available for contributing to a retirement plan.

Also read: What Should I Do If My Employer Won’t Provide A Pay Stub?

Fund Your FSA

For taxpayers who don’t have high deductible health coverage it is possible to pay medical costs from a Flexible Spending Account or FSA. Some employers offer these accounts, which are funded by pre-tax contributions.

The limit that you can contribute to an FSA is $2,850 per year, and it must be used before the end of the calendar year or the balance may be forfeited.

Some employers may let you carry money over to the next year. If not, you can use it for everyday medical needs such as bandages, pregnancy test kits, or other useful medical supplies.

Many companies offer dependent care as part of a Flexible Savings Account up to a limit of $5,000. Unlike an HSA, you cannot take an FSA with you when you change jobs.

Also read: Do You Need Multiple W2 Forms From The Same Employer?

Make Charitable Donations

Charitable donations are deductible and can lower the amount of your tax liability. Your contributions don’t even have to be in cash, although of course you can make dollar donations.

Anything that you donate, including clothes, food, household items, or sporting goods, can be deducted. However, it has to be donated to a bona fide charity, and you will need to provide a receipt.

The amount that you can deduct for charitable donations is $300, or for married couples who file jointly, the limit is $600. You will need to itemize to claim this deduction rather than taking the standard deduction. If you’re curious about whether charitable contributions are truly a wise financial strategy, you can explore how charitable giving fits into smart financial planning to maximize both your impact and your tax benefits.

Check Your Eligibility For EITC

An income tax credit is a reduction in your actual tax bill rather than a deduction, which just lowers the amount of your taxable income.

The Earned Income Tax Credit is a refundable tax credit. Even if you don’t have to pay any federal income tax, you could still qualify for this tax credit, which is worth $6,728.

It is calculated based on income from $21,430 for single taxpayers with no children up to $57,414 for married couples who file jointly and have three or more children.

Also read: Cost Of Living By State In USA

Itemize State Sales Tax Or State Income Tax

Taxpayers who itemize deductions rather than taking the standard deduction can include state sales tax, or if it applies, state income tax.

For those living in a state that does not levy income tax deductions or state sales tax is a good alternative, especially if you have made a large purchase during the year, such as a car, boat or engagement ring.

If you live in a state that imposes income tax, you can deduct this against federal tax, but you will not be able to deduct both state sales tax and state income tax. This itemized deduction has to be filed on Schedule A of Form 1040.

There is a cap of $10,000 for state income tax on federal tax from all sources.

Final Thoughts

These seven methods of saving tax on your salary are just some of the ways that you can reduce your tax liability.

All of these means of saving tax are completely legitimate ways to save yourself some money on your taxes.

This is not an exhaustive list, and there are other options, some of which will depend on individual circumstances.

It is imperative that people can access their pay stubs so they can keep them for their own records.

- 1. Enter Your Information

- 2. Select Your Favorite Theme

- 3. Download Your Stub!

![How To Save Tax On Your Salary [7 Methods]](https://www.thepaystubs.com/cms-uploads/media/cache/author_article/files/cms/writers/thumbnail/606203657443e953830870.jpeg)